The first step in the tax research process is to establish all of the facts and circumstances provided by your client in order to determine which tax laws apply to your client’s fact pattern. At this initial stage, it is imperative not to omit nor overlook any of your client’s facts and circumstances whether appearing material or immaterial. Always be guided by the axiom that facts and circumstances appearing to be immaterial individually may, in fact, be material in the aggregate.

The third step in the tax research process entails identifying the specific authorities to support all of your client’s tax issues while appropriately weighing authorities that may be contrary to your supporting position. Generally, this process begins with consulting statutory authority (e.g., the Internal Revenue Code) and quickly expands to encompass administrative authority (e.g., Proposed Treasury Regulations, Temporary Treasury Regulations, Final Treasury Regulations, Revenue Rulings, Revenue Procedures, Private Letter Rulings, Technical Advice Memorandum, General Counsel Memorandum, Circular 230, Internal Revenue Manual, Internal Revenue Bulletins, IRS Field Service Advice Memorandum, IRS Determination Letters, and IRS Notices, etc.) and judicial authority (e.g., judicial interpretations decided by the U.S. Tax Court, the U.S. District Court, the U.S. Court of Federal Claims, the U.S. Circuit Court of Appeals, the U.S. Court of Appeals for the Federal Circuit, and the U.S. Supreme Court). In addition, at times, you the tax professional may have to consult the legislative history (e.g., the Public Laws and Congressional Committee Reports from the House of Representatives and the Senate) of a particular Internal Revenue Code section to fully address what Congress’s intent was in passing a particular bill. Lastly, you may also want to consult the voluminous range of editorial interpretations (e.g., Tax Treatises, Tax Journals, etc.) available to assist in the interpretation a particular tax issue. However, it must be duly noted that editorial interpretations are impermissible sources of authority before the Service and the judicial system. For clarification purposes, the subsequent synopsis will elaborate upon the aforementioned statutory, administrative, and judicial interpretations:

All federal level tax statutes passed by Congress into law are compiled and published in Title 26 of The United States Code. As it should be recalled, Title 26 of The United States Code contains the specific statutes that authorize the Service to collect taxes for the federal government. Generally, the tax research process begins with consulting the Internal Revenue Code and quickly expands to encompass administrative and judicial authorities based upon the complexity of the tax issue under analysis.

The Treasury Regulations provide the official interpretations of the Internal Revenue Code by the Treasury Department and have the force and effect of law. The most common forms of Treasury Regulations include:

A Revenue Ruling is an official interpretation by the Service of the tax laws. Initially, Revenue Rulings are published in the weekly Internal Revenue Bulletin. The same rulings later appear in the permanently bound Cumulative Bulletin, a semi-annual publication of the Government Printing Office. Revenue Rulings hold less weight than the Treasury Regulations because they are intended to cover only specific fact patterns. Regardless, Revenue Rulings can provide valid precedent but only if your client’s facts and circumstances are substantially identical.

A Revenue Procedure is a statement of procedure that affects the rights or duties of taxpayers or other members of the public under the Code. Similar to Revenue Rulings, Revenue Procedures are less authoritative than Treasury Regulations. However, Revenue Procedures should be binding on the Service and may be relied upon by taxpayers.

Private Letter Rulings (hereinafter “PLR”) are issued directly to taxpayers who formally request and pay for advice about the tax consequences applicable to a specific business transaction. Such PLR request have been employed frequently by either taxpayers themselves or the taxpayer’s representatives (e.g., a taxpayers’ representation through a CPA Firm or Law Firm) to assure themselves of a pre-planned tax result before they consummate a transaction and as a subsequent aid in the preparation of the tax return’s filing position. When the IRS issues a PLR it is understood that the PLR is limited in scope and application to the taxpayer making the request.

A Technical Advice Memorandum (hereinafter “TAM”) is a special after-the-fact ruling that may be requested from the taxpayer or the technical staff of the Service. For instance, if a disagreement arises in the course of an audit between the taxpayer or the taxpayer’s representative and the revenue agent, either side may request formal technical advice on the issues(s) through the District Director. Under certain circumstances, TAM’s can be used as a basis for the issuance of a Revenue Ruling and can also be subsequently published as a PLR.

General Counsel Memorandum (hereinafter “GCM”) are legal memorandum that are prepared by the IRS Chief Counsel’s Office. GCM’s analyze proposed Revenue Rulings, Private letter Rulings, and Technical Advice Memorandum. GCM’s that were issued after 1981 constitute substantial authority for purposes of the penalty assessed for the substantial understatement of income tax.

Circular 230 is an IRS publication that sets forth the requirements and responsibilities of professionals (e.g., Attorneys, Certified Public Accountants, Enrolled Agents, and Enrolled Actuaries) admitted to practice before the Service. It should be duly noted that Circular 230 was most recently revised on June 12, 2014 and all tax professionals admitted to practice before the Service must adhere to.

The Internal Revenue Manual (hereinafter “IRM”) is an official compilation of policies, procedures, instructions, and guidelines for the organization, function, operation and administration of the Service. It is not legally binding and the policies are not mandatory. The IRM guidelines do not confer any rights on taxpayers.

IRS Field Service Advice (hereinafter “FSA”) are taxpayer specific rulings furnished by the IRS National Office in response to requests made by the taxpayers or IRS Officials.

A Determination Letter is issued by the IRS at the taxpayer’s request to outline the Service’s position on a particular transaction that has already been completed. Generally, Determination Letters are issued only when a determination can be made on the basis of clearly established rules in the statute or regulations.

When prompt guidance concerning an item of the tax law is needed, the IRS publishes notices in the Internal Revenue Bulletin. These notices are intended to be relied upon by the taxpayers to the same extent as a Revenue Ruling or Revenue Procedure.

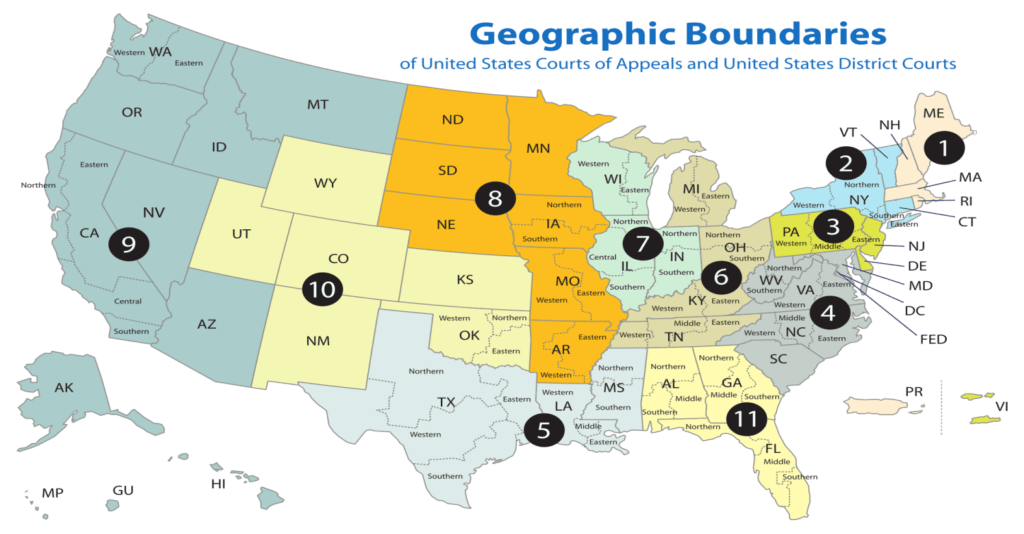

The U.S. Tax Court is an independent 19 judge federal administrative agency that functions as a court to hear appeals by taxpayers from adverse administrative decisions by the Service.

The U.S. District Court hears civil actions against the United States for the recovery of any tax alleged to have been erroneously or illegally assessed or collected by the Service. Trial by jury is available at the preference of either the petitioner or defendant.

The U.S. Court of Federal Claims is a Washington D.C. based appellate-level court in which a taxpayer may sue the government for a refund of overpaid taxes.

The U.S. Court of Appeals is one of thirteen courts including the District of Columbia and the Federal Circuit Courts, to which appeals from a trial court, such as the U.S. Tax Court, are directed.

The U.S. Court of Appeals for the Federal Circuit hears appeals from the U.S. Court of Federal Claims.

The U.S. Supreme Court is the highest appellate court in the federal court system and in most states. The U.S. Supreme Court, under its certiorari procedure authority, reviews the constitutionality of a tax law and a small number of tax decisions by the Court of Appeals.

The subsequent chart illustrates the geographic boundaries of The United States Courts of Appeals and the United States District Courts:

The fourth step in the tax research process entails the resolution of your client’s tax issues after identifying, analyzing, and interpreting all of the applicable authorities. It cannot be overstated that you should have provided, as needed, reasonable statutory, administrative, and judicial support to demonstrate that your tax return filing position could be upheld if challenged by the Service upon the fruition of an examination and that you exercised due diligence and acted in good faith. Furthermore, at times, positions taken on tax returns may need to be disclosed on Form 8275 entitled “Disclosure Statement” or Form 8275-R entitled “Regulation Disclosure Statement” depending upon the complexity and controversial nature of the tax issue. Noting, by disclosing positions on your client’s tax returns you may be able to avoid paid preparer penalties should your position be disallowed and avoid the application of the six year statutory period for assessment under I.R.C. § 6501(e).

From a risk management perspective, in order to mitigate or avoid income tax return paid preparer penalties pursuant to I.R.C. § 6694 (e.g., penalties that are assessed on both paid tax return preparers and tax advisers that are deemed paid tax return preparers due to their consulting on matters that constitute a substantial portion of their client’s tax returns even if they were not engaged to prepare nor review the tax return), a “More-Likely-Than-Not” standard should be satisfied. The subsequent standards of the applicable levels of opinions should be scrupulously analyzed when assessing your tax return filing position:

It should be duly noted that each of the aforementioned standards above has a relevant meaning to both the taxpayers and tax professionals when evaluating a tax position and the related disclosure requirements. Noting, the percentages listed for “More-Likely-Than-Not” and “Realistic Possibility of Success” are specifically provided for and discussed in the treasury regulations. In contrast, the percentages for “Substantial Authority”, “Reasonable Basis”, “Non-Frivolous”, “Frivolous” have been developed based upon their relative importance in the hierarchy of standards of opinion as principally provided for in congressional committee reports. Moreover, while not mathematically calculable, the percentages are still practical in demonstrating the relative strength of one level as opposed to another level.

The fifth and final step in the tax research process entails communicating the conclusion to your client. Your client, of course, must ultimately make the final decision concerning what course of action to take, even though the client’s decision is guided by and often dependent upon the conclusions reached by you, the tax professional. It is strongly recommended that this tax advice be rendered to your client in a written format, as opposed to verbal communication, and preferably in a formal tax advice memorandum format (e.g., Facts & Circumstances Section; Issue(s) Section; Analysis Section; and Conclusion Section) meticulously discussing the applicable statutory, administrative, and judicial authority to appropriately document your due diligence in assessing the tax issues(s) and resolving them satisfactorily to reach a strong tax return filing position (e.g., “More-Likely-Than-Not”, “Should”, “or “Will” filing positions). Finally, caveat language in the form of a disclaimer should be documented within the tax advice memorandum for any areas of the tax law that were not within the scope and application of your tax research services (e.g., the scope and application of our tax advice memorandum is in connection to the U.S. Federal-level tax consequences only and does not provide any advice or analysis in connection to any U.S. Multi-State tax consequences nor any advice in connection to Financial Statement Reporting purposes under U.S. GAAP nor IFRS).

By following the preceding all-inclusive practical steps in the tax research process you should be able to render your tax research services to your entire client base in a more efficient, effective, and productive manner while adequately weighing risk management concerns in connection to tax return filing positions. As a final reminder, the guidance contained in this article should be applied with due professional care including seeking further professional advice from a subject matter expert should it be deemed warranted based upon both the complexity and contentious nature (e.g., taking a tax position contrary to a Treasury Regulation on Form 8275-R, etc.) of the tax matter under review.

This article originally appeared in TaxConnections March Issue.

Embrace the power of tax credit savings with Source Advisors and propel your business towards growth and success. Partner with us today to unlock your company’s full potential.