Tax News

The One Big Beautiful Bill Passes Senate: What CPAs Need to Stay Ahead

The One Big Beautiful Bill is Ready for the President’s Signature: What CPAs Need to Stay Ahead The One Big

The One Big Beautiful Bill Act

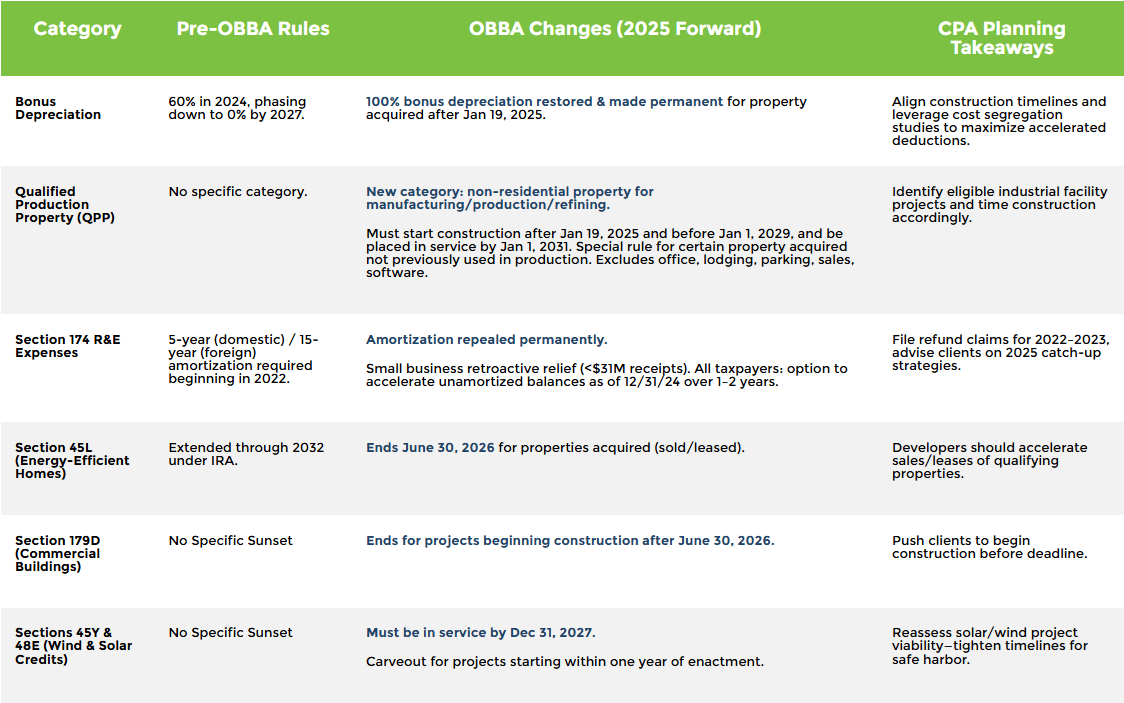

The One Big Beautiful Bill Act (OBBBA) introduces sweeping changes that affect depreciation planning, R&D expensing, and energy incentives. Some provisions—like the permanent return of 100% bonus depreciation—create long-term opportunities, while others—such as the shortened windows for Section 45L, 179D, and clean energy credits—require immediate action.

The comparison chart below highlights the key before-and-after rules and outlines the planning takeaways CPAs should discuss with clients to ensure they capture benefits before deadlines close.

| Category | Pre-OBBA Rules | OBBA Changes (2025 Forward) | CPA Planning Takeaways |

|---|---|---|---|

|

Bonus Depreciation |

60% in 2024, phasing down to 0% by 2027. |

100% bonus depreciation restored & made permanent for property acquired after Jan 19, 2025. |

Align construction timelines and leverage cost segregation studies to maximize accelerated deductions. |

|

Qualified Production Property (QPP) |

No specific category. |

New category: non-residential property for manufacturing/production/refining. Must start construction after Jan 19, 2025 and before Jan 1, 2029, and be placed in service by Jan 1, 2031. Special rule for certain property acquired not previously used in production. Excludes office, lodging, parking, sales, software. |

Identify eligible industrial facility projects and time construction accordingly. |

|

Section 174 R&E Expenses |

5-year (domestic) / 15-year (foreign) amortization required beginning in 2022. |

Amortization repealed permanently. Small business retroactive relief (<$31M receipts). All taxpayers: option to accelerate unamortized balances as of 12/31/24 over 1–2 years. |

File refund claims for 2022–2023, advise clients on 2025 catch-up strategies. |

|

Section 45L (Energy-Efficient Homes) |

Extended through 2032 under IRA. |

Ends June 30, 2026 for properties acquired (sold/leased). |

Developers should accelerate sales/leases of qualifying properties. |

|

Section 179D (Commercial Buildings) |

No Specific Sunset |

Ends for projects beginning construction after June 30, 2026. |

Push clients to begin construction before deadline. |

|

Sections 45Y & 48E (Wind & Solar Credits) |

No Specific Sunset |

Must be in service by Dec 31, 2027. Carveout for projects starting within one year of enactment. |

Reassess solar/wind project viability—tighten timelines for safe harbor. |

Embrace the power of tax credit savings with Source Advisors and propel your business towards growth and success. Partner with us today to unlock your company’s full potential.

The One Big Beautiful Bill is Ready for the President’s Signature: What CPAs Need to Stay Ahead The One Big

IRS Issues New Guidance on Beginning of Construction Rules for Wind and Solar Tax Credits The Treasury Department and IRS

A Guide to Qualified Production Property (QPP) The One Big Beautiful Bill Act (OBBB) introduces IRC § 168(n), establishing a

The One Big Beautiful Bill is Ready for the President’s

A Guide to Qualified Production Property (QPP) The One Big

IRS Issues New Guidance on Beginning of Construction Rules for