Inventory valuation is an accounting process used by companies to assign value to their inventory. It determines the cost of unsold goods at the close of an accounting period and plays a critical role in calculating the cost of goods sold (COGS) and the gross profit for the period.

The main reason for this process is to assign a monetary value for a company’s inventory items at the close of a reporting period. There are several methods used for inventory valuation. Each method affects the financial statements differently, especially under varying market conditions.

Advantages of LIFO

The LIFO (Last-In, First-Out) accounting method assumes that the inventory items most recently purchased are the first ones sold or used, which means that the COGS is calculated using the most recent inventory costs, leaving older inventory costs in the ending inventory balance.

Tax Savings & Cash Flow Improvement

LIFO can lead to lower cost of goods sold (COGS) during inflation.

LIFO can result in lower taxable income in times of inflation because it matches higher current prices with current sales, thereby reducing reported profits and tax liabilities.

Cash flow can be improved by deferring taxes since LIFO reports lower profits in times of rising prices.

Disadvantages of LIFO

Although there are several benefits to using the LIFO accounting method, there are also disadvantages that are important to note.

LIFO may not reflect the actual cost of remaining inventory, especially during periods of inflation.

LIFO calculations can be more complex compared to FIFO (First-In-First-Out). Because of the complexities of this method, there will potentially be a need for additional record-keeping.

LIFO is not allowed under some international accounting standards (IFRS).

Disadvantages of LIFO

Although there are several benefits to using the LIFO accounting method, there are also disadvantages that are important to note.

LIFO may not reflect the actual cost of remaining inventory, especially during periods of inflation.

LIFO calculations can be more complex compared to FIFO (First-In-First-Out). Because of the complexities of this method, there will potentially be a need for additional record-keeping.

LIFO is not allowed under some international accounting standards (IFRS).

Because of the pros and cons of this accounting method, it is critical for businesses to select a provider that understands the complexities of LIFO and that has a deep understanding of their financial goals. With Source Advisors as a trusted partner, businesses can tap into the nuances of this method and determine whether it fits into their overall business strategy.

Inventory identification is a crucial aspect of managing a company’s finances. It impacts your cost of goods sold (COGS), profitability, and ultimately, your tax burden. Two prominent inventory identification methods are LIFO (Last-In, First-Out) and FIFO (First-In, First-Out). Each method comes with its own set of advantages and disadvantages, and understanding these differences is essential for making informed decisions for your business.

Inventory identification is a crucial aspect of managing a company’s finances. It impacts your cost of goods sold (COGS), profitability, and ultimately, your tax burden. Two prominent inventory identification methods are LIFO (Last-In, First-Out) and FIFO (First-In, First-Out). Each method comes with its own set of advantages and disadvantages, and understanding these differences is essential for making informed decisions for your business.

LIFO vs FIFO: When to Use Which

Both LIFO and FIFO offer tax advantages and disadvantages. LIFO can help businesses reduce their tax liability in times of rising costs, as it allows them to match higher costs with current revenues. FIFO, on the other hand, provides a more accurate representation of the actual cost of goods sold but may result in higher taxes during inflation.

Deciding the optimal method depends on your unique business. Here are some things to consider:

1. Industry Spice:

Is your industry prone to fluctuating costs, like oil & gas? LIFO might be your flavor. Stable industries like retail often prefer FIFO’s simplicity.

2. Price Trends:

Are prices rising, falling, or steady? LIFO shines in inflationary times, while FIFO is better for deflationary periods.

3. Financial Reporting Transparency:

FIFO often provides a clearer picture in your financial statements in terms of comparability, essential for investors and stakeholders.

How LIFO and FIFO can impact business profitability and financial stability:

LIFO can result in lower taxable income, but it may not accurately reflect the true value of inventory in times of inflation.

FIFO can provide a more accurate representation of inventory value, but it may lead to higher tax liabilities.

In the end, businesses should carefully evaluate their specific circumstances, consult with accounting professionals, and consider the long-term implications before deciding whether to use LIFO or FIFO. By making an informed choice, companies can effectively manage their inventory, optimize profitability, and maintain financial stability.

While inflation is not at the high levels seen in the last couple of years, if you haven’t elected LIFO previously, now is the time to look at Last-In-First-Out (LIFO) accounting. If you have inventories of machinery and equipment, glass products or any concrete or cement inventory, there could be tax savings available for 2023. Whether you are already on LIFO or not, analyzing the IPIC LIFO method could be a great opportunity. IPIC LIFO uses indexes published by the Bureau of Labor Statics to measure inflation on your inventory. In 2023 these indexes show inflation is still on the rise in many industries, which means businesses of all sizes could experience tax savings using LIFO.

Whether you are a manufacturer, distributor, or retailer, you have the opportunity to mitigate the negative impact of price increases and annually save money by using the LIFO inventory method. Adopting LIFO removes the phantom profits caused by inflation, lowering your tax liability and creating cash for reinvestment in your business. Any business with over $2M in inventory that is experiencing inflation is a qualified candidate for electing LIFO. Depending on the inflation rate and the inventory level, the cash savings can be quite substantial.

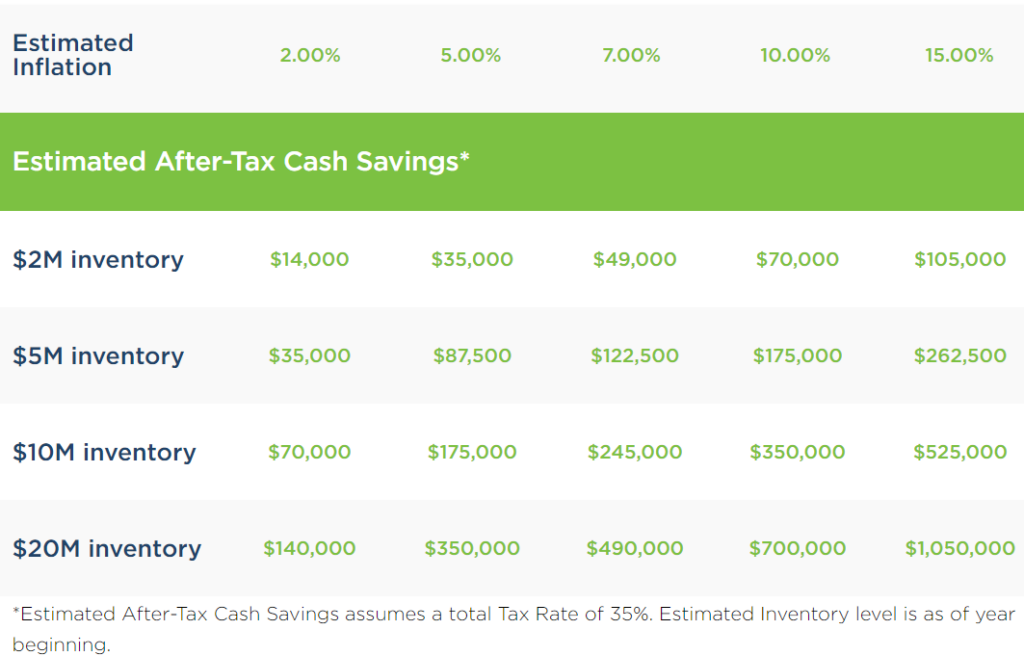

Tax Benefit Projections

Tax Benefit Projections

Estimated Inflation

2.00%

5.00%

7.00%

10.00%

15.00%

Estimated After-Tax Cash Savings*

$2M inventory

$14,000

$35,000

$49,000

$70,000

$105,000

$5M inventory

$35,000

$87,500

$122,500

$175,000

$262,500

$10M inventory

$70,000

$175,000

$245,000

$350,000

$525,000

$20M inventory

$140,000

$350,000

$490,000

$700,000

$1,050,000

*Estimated After-Tax Cash Savings assumes a total Tax Rate of 35%. Estimated Inventory level is as of year beginning.

Case Studies

A wine distributor with $30m in inventory is planning to elect LIFO in 2023 as there is currently about 7% inflation in their inventory. Assuming inflation holds steady through the end of the year, they will calculate LIFO reserve of almost $2m, providing tax savings of over $650,000. Knowing this projected savings now helps them as they begin tax planning for 2023.

Inflation for sporting goods is currently about 10%. A family-owned store with $2m in prior year inventory that elects LIFO in 2023 can expect a first year LIFO reserve of over $200,000, translating to more than $70,000 in tax savings.

Taxpayers across the different industries and with inventory can save tax dollars with LIFO.

Taxpayer Type

Estimated

2023 Inflation

Prior Year

Inventory Value

Year

1 LIFO Reserve

After-tax

Cash Savings*

Industrial Products Manufacturer

4%

$3,000,000

$117,000

$40,950

Machinery and Equipment Retailer

6%

$12,000,000

$660,000

$244,200

Sporting Goods Store

11%

$4,000,000

$440,000

$162,800

Aircraft Engine Manufacturer

5%

$14,000,000

$700,000

$259,000

Lawn & Garden Store

4%

$6,000,000

$240,000

$88,800

Glass Bottles Distributor

10%

$5,000,000

$480,000

$177,600

Packaged Concrete Manufacturer

12%

$10,000,000

$1,200,000

$444,000

*After tax-cash savings is measured using 35% tax rate.*

An analysis of LIFO benefits is seamless and is provided at no cost to you. Just send a copy of the year beginning and year ending inventory files, including unit costs, and we’ll provide a free estimate of benefit and a price quote for the project.

*After tax-cash savings is measured using 35% tax rate.*

An analysis of LIFO benefits is seamless and is provided at no cost to you. Just send a copy of the year beginning and year ending inventory files, including unit costs, and we’ll provide a free estimate of benefit and a price quote for the project.

Understanding LIFO as an effective mitigation strategy for inflation is an economic challenge that significantly impacts a wide range of businesses, from manufacturers and distributors to retailers. Amidst the challenge of rising costs for raw materials and finished goods, the Last-In-First-Out (LIFO) inventory method emerges as a potent strategy to navigate this tricky economic landscape.

How LIFO Contributes to Tax Savings

At its core, LIFO operates by matching the costs of goods sold with the most recent, and typically higher, costs, while the oldest costs remain tied to unsold inventory. This process results in a higher cost of goods sold, which in turn translates into lower taxable income, thereby reducing tax liability. This mechanism helps businesses effectively combat the adverse effects of inflation.

The Criteria for Adopting LIFO

Adoption of the LIFO method isn’t universal. It’s particularly beneficial for businesses experiencing inflation and maintaining an inventory valued at over $2M. The potential for significant tax savings, achieved annually, transforms LIFO into a sustainable method to manage the potential repercussions of inflation.

The Power of Reinvestment with LIFO

The use of the LIFO method not only provides tax relief but also frees up valuable cash flow for businesses. By lowering tax liabilities, these extra funds can be funneled back into the business, leading to reinvestment opportunities. These might include investing in technological upgrades, expanding the workforce, or scaling operations, thereby further enhancing business growth.

Adopting LIFO

The decision to adopt LIFO requires careful and strategic consideration of the client’s inventory flow and overall financial position. It’s not a one-size-fits-all solution. However, if a client qualifies, LIFO can emerge as a powerful tool to help combat the negative effects of inflation, strengthening their financial resilience.

LIFO represents an effective strategy that can help businesses counteract the impact of inflation, lower tax liabilities, and create opportunities for reinvestment. At Source Advisors, we stand ready to provide expert guidance on navigating this complex yet highly beneficial financial planning tool.